Counter market volatility with Income America 5ForLife

Stock market volatility is a normal part of investing, but that doesn't make it any easier for participants who are anxiously watching their retirement plan portfolios rise and fall.

In fact, assuming a 50-year investment horizon, participants can expect to experience roughly 14 bear markets1—when the closing price of the stock market drops at least 20% from its most recent high.

Beyond market volatility, there's always the threat of a recession. Since 1948, the United States has lived through 19 recessions2, triggered by everything from railroad failures to inflation to the dot-com bust.

While higher market volatility means higher investment risk, it also means potentially greater earnings potential. That's why some investors are content to ride out the ups and downs of the market while they're still working. However, market volatility in retirement is another story.

Hanging on through market volatility

In volatile markets, prices can rise and fall rapidly, which can sometimes cause participants to make rash decisions, such as panic-selling their investments. And even a single misguided investment decision can have major ramifications on participants' financial security and income in retirement.

Participants who are nearing or already in retirement are especially vulnerable to stock market volatility. That's because when participants sell investments to fund their lifestyle by taking income from their portfolio, these unrealized "paper losses" become real. In particular, significant market declines early in a participant's retirement can have dramatic "sequence of returns risk" ramifications on the longevity of a retirement investment portfolio.

Choosing steady retirement income over stock market volatility

Instead of being at the whim of the stock market in retirement, participants now have a more predictable option: Income America™ 5ForLife. By offering this series of target date portfolios in a retirement plan's lineup, you can help plan participants limit their exposure to market volatility and enjoy guaranteed retirement income for life.

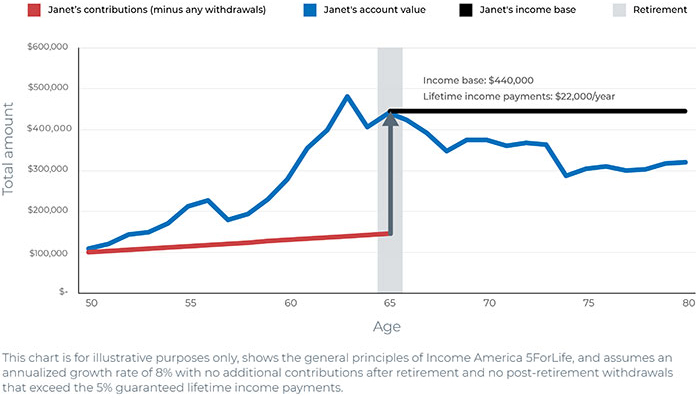

Here's how it works. Participants contribute to the in-plan Income America 5ForLife investment option, just like any other investment in the retirement plan lineup. When they turn 65, their income base (which is used to calculate their guaranteed retirement income amount) is set and can never go down, even if the market drops. Participants can then begin receiving lifetime income payments of 5% of their income base every year for the rest of their lives—guaranteed.3

Consider this retirement income example: Janet has an income base of $440,000. When she turns 65, she receives 5% of that amount ($22,000) each year for life, even if the market drops. With Income America 5ForLife, Janet can count on having a steady stream of income in retirement despite market volatility.

Help your participants save for a future they can depend on

Participants are ready for a more secure future. In fact, research shows that 80% of participants would be more likely to leave money in their retirement plan if their employer offered an investment option specifically to help retirees draw income during retirement.

Consider adding Income America 5ForLife to the plan's investment lineup to provide participants with guaranteed retirement income and protection from stock market volatility.

1 A Brief History of U.S. Bear Markets, Investopedia.com, September 23, 2022

2 History of Recessions in the United States, thebalancemoney.com, October 19, 2022

3 The income guarantee is based on the income base at age 65, which is set to the greater of market value or participant contributions (less withdrawals) to date. The market value of the account is never guaranteed and fluctuates based on investment performance. To receive the guaranteed income, a participant must stay invested in Income America 5ForLife. If the participant withdraws more than the guaranteed annual income in any year, their income base and future guaranteed annual income amount will decrease. If the joint option is elected, the payout will be lower than 5%, depending on the participant's age and their spouse's age. Guarantees are subject to the claims-paying ability of the issuing companies.

Keep reading:

- Income America releases a new retirement income video series: "On the Money"

- Why Income America 5ForLife might make an ideal qualified default investment alternative (QDIA)

- Five reasons registered investment advisors may recommend Income America 5ForLife

- Retirement portfolios made simple

- Help employees manage sequence of returns risk in their retirement portfolios